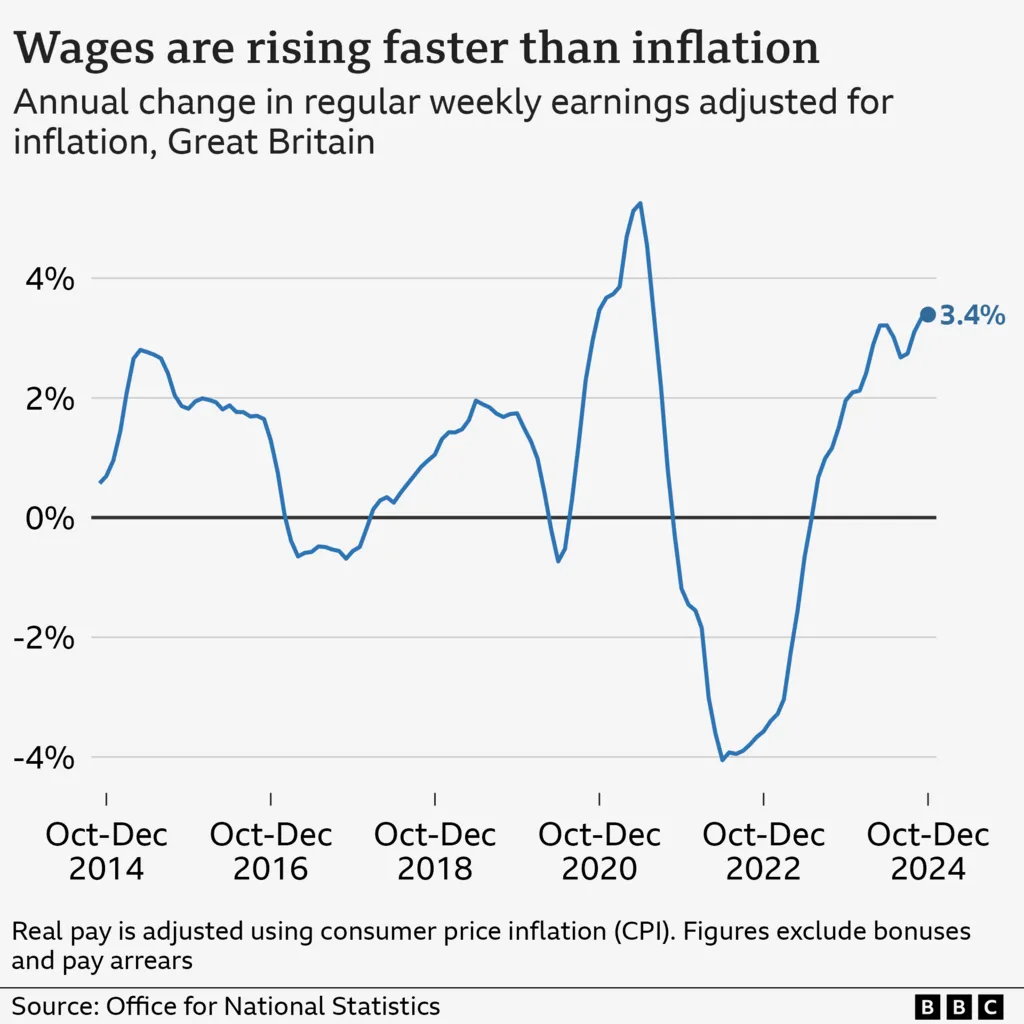

Official data indicates that UK wages are rising faster than inflation, with earnings increasing for both public and private sector employees.

Between October and December, real wages—adjusted for inflation—grew by 3.4% compared to the same period in the previous year, according to the Office for National Statistics (ONS).

Unemployment remained steady at 4.4%, but the ONS cautioned that its employment data may be less reliable due to lower survey response rates.

Meanwhile, businesses have warned of potential job cuts and price hikes ahead of rising employment costs in April. Employers have expressed concerns that increased National Insurance payments, higher minimum wages, and reduced business rates relief could limit future pay growth and impact investment.

Excluding inflation, annual pay growth—excluding bonuses—stood at 5.9% from October to December, up from 5.6% previously. Private sector earnings rose by 6.2%, while public sector wages increased by 4.7%.

Inflation, which measures the rate of consumer price increases, stood at 2.5% in December but is expected to rise due to higher energy and water costs.

Yael Selfin, chief economist at KPMG UK, predicted a gradual slowdown in wage growth in the coming months.

Some economists noted that a slight increase in private sector wages, closely monitored by the Bank of England for interest rate decisions, is unlikely to prompt significant policy changes.

Earlier this month, the Bank of England reduced interest rates from 4.75% to 4.5%. Rob Wood, of Pantheon Macroeconomics, suggested that policymakers would remain cautious about further rate cuts given the recent wage growth trends.

Ms. Selfin noted that hiring intentions among businesses had “weakened significantly,” with the hospitality and retail sectors expected to be hit hardest by upcoming cost increases due to their reliance on lower-wage workers.

Jane Gratton, deputy director of Public Policy at the British Chambers of Commerce, warned that businesses can only absorb so many additional costs before employment and investment opportunities are impacted. She urged the government to minimize business costs and ensure access to a skilled, healthy workforce.

From April, employers will pay 15% in National Insurance on salaries above £5,000, up from the current 13.8% on earnings over £9,100.

The Treasury maintains that its Budget measures will provide businesses with stability for investment and growth. However, concerns persist that corporate cutbacks could slow UK economic expansion, a key government priority for improving living standards.

A recent survey suggested companies may raise prices to offset rising costs, which could push inflation higher in the coming months and add pressure to household budgets.

The ONS reported that total job vacancies declined by 110,000 (11.8%) compared to the previous year but remain above pre-pandemic levels. Payroll employment rose by 21,000 in January, reaching 30.4 million.

Chris Eldridge, CEO for UK, Ireland, and North America at Robert Walters, said the job market outlook remains uncertain. He pointed to late March as a key test, when National Insurance changes take effect alongside potential developments in the Employment Rights Bill.