On Thursday, rising oil prices assisted in stock market gains as China made its latest effort to boost its faltering economy and the European Central Bank hinted that its tenth consecutive increase in interest rates would be its last for some time.

Although both the euro and yuan plummeted against the dollar following the actions of their respective central banks, a more than 3% increase in Europe’s oil, gas, and mining equities (.SXPP) meant that response to the ECB’s hike was minimal.

On Thursday, rising oil prices assisted in stock market gains as China made its latest effort to boost its faltering economy and the European Central Bank hinted that its tenth consecutive increase in interest rates would be its last for some time.

Although both the euro and yuan plummeted against the dollar following the actions of their respective central banks, a more than 3% increase in Europe’s oil, gas, and mining equities (.SXPP) meant that response to the ECB’s hike was minimal.

In contrast, the People’s Bank of China decreased its reserve requirement ratio (RRR) by 25 basis points, after cuts to two of its other important policy rates over the previous month as Beijing’s authorities sought to aid.

Gilles Moec, chief economist of Axa, commented on the ECB’s upcoming news conference by saying: “How they manage the forward guidance is going to be interesting.”

He continued, “If they continue to sound deeply concerned about inflation, the market may experience some difficulties.” If you are concerned about pay trends, you have more cause for concern now than you did six months ago because core inflation has not really slowed down.

Even while stock markets were generally rising, the trend wasn’t linear.

European automakers (.SXAP) were forced to go backwards after Beijing denounced Wednesday’s investigation by Brussels into electric vehicle subsidies as “naked” protectionism.

As anticipation for more U.S. rate hikes in the coming months grew due to strong retail sales and producer pricing data, S&P 500 futures likewise gave up some of their gains in New York.

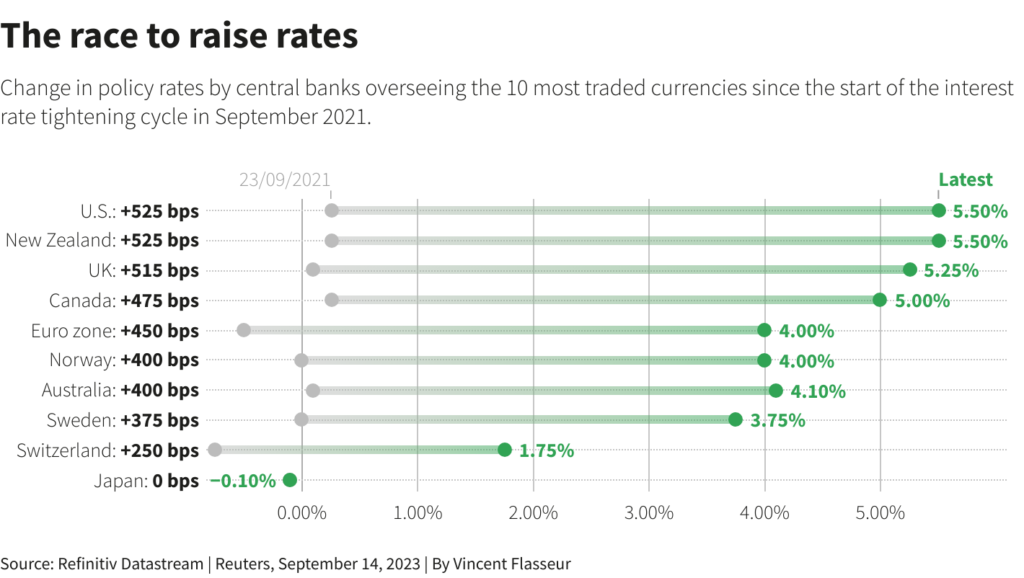

The ECB, which serves as the central bank for the 20 nations that use the euro, was in a difficult situation. Even after its wave of rate increases, prices are still rising at a rate that is more than twice its 2% target, and it will take another two years for them to return to that level.

Investors had been leaning towards a halt following a recent string of unfavorable data until Reuters reported on Tuesday that the bank’s updated staff predictions would increase the inflation forecast for next year to over 3% once more.

They said on Thursday that inflation is now anticipated to be 5.6% in 2023, 3.2% in 2024, and 2.1% in 2025.

In the meantime, the growth outlook has worsened, and the ECB now projects a 0.7% increase in 2023, down from its earlier forecast of 0.9%. The economy will expand by 1.0% in the upcoming year, with no significant increase anticipated.

The benchmark for borrowing costs in the euro region, the 10-year government bond yield from Germany, was recently down 4 basis points (bps) at 2.613%. Just before to the decision, the yield, which changes inversely to the bond’s price, was 2.638%.

Nadia Calvino, Spain’s economy minister, told reporters in Santiago de Compostela, “We hope that it will be clear from (their explanations) that this hike puts an end to the rapid increase in interest rates that we have seen over the last year.”

CARS SKID

The stock market’s movements on Wednesday’s statement that the European Commission was looking into subsidies given by China to increasingly powerful electric car manufacturers like BYD revealed how investors were processing the news.

Overnight, Beijing reacted, labeling the action “a naked protectionist act” and warning that the EV investigation will deteriorate relations with the EU.

BMW (BMWG.DE), Volkswagen (VOWG_p.DE), Mercedes (MBGn.DE), and Fiat and Peugeot producer Stellantis (STLAM.MI) were all down between 1% and 2% as analysts predicted a tit-for-tat tariff battle.

The possibility of retribution in China “should not be ignored” for German OEMs, according to UBS analysts.

Even if there had been less of an impact elsewhere in Asia, China’s automakers had experienced a decline over night.

For its best session in a week and a half, MSCI’s largest index of Asia-Pacific equities outside of Japan (.MIAPJ0000PUS) increased 0.6%.

Nikkei (.N225) of Tokyo increased 1.4% to a one-week high. The BSE Sensex (.BSESN) index in India increased by 0.5% to a new record high, and S&P 500 futures gained as much as 0.3%.

According to data released on Wednesday, increasing fuel costs increased headline consumer prices in the United States by the most in 14 months in August, coming in at a slightly higher-than-expected 3.7% annual rate. As predicted, core inflation fell to an annual rate of 4.3%.

Both the U.S. currency and Treasury yields originally surged upward before they both reversed course. Fed funds futures barely changed and indicate a 45% possibility of another rate hike by the end of the year and almost no chance of one next week.

SHOT IN THE ARM

The dollar increased once more on the currency exchange markets.

As traders anticipate any exit being gradual and the gap with U.S. rates staying broad, the yen has mostly given back gains it had made after Bank of Japan Governor Kazuo Ueda hinted at the conditions for an end to negative short-term rates.

Along with the RRR reduction on Thursday, the central bank of China has also requested that some of the largest lenders in the nation hold off from promptly squaring their foreign exchange positions in the market, according to two persons with knowledge of the situation who spoke to Reuters.

Arm Holdings (ARM.O), a company that designs chips, will be a major focus for stock markets when it starts trading in New York today after being valued at $54.5 billion thanks to the largest share float of the year so far at $51 per share.

As Saudi Arabia and Russia prolong production restrictions to the end of 2023, oil prices are rising. Brent crude futures were up 1.5% on the day at little over $93 per barrel in London, bringing their three-month gain to 30%.

If cuts are continued into the first half of next year, experts at ANZ Bank predicted that Brent prices might reach $100. “The market remains beholden to Saudi Arabia’s oil policy,” they added.